The 9 Multiple Movers

What Really Drives Pricing In An Acquisition

TL;DR

Two levers move the price on an acquisition: cash flow and the multiple sitting on top of it.

Most owners work cash flow their whole careers. The multiple is the bigger lever, and it doesn’t move on its own.

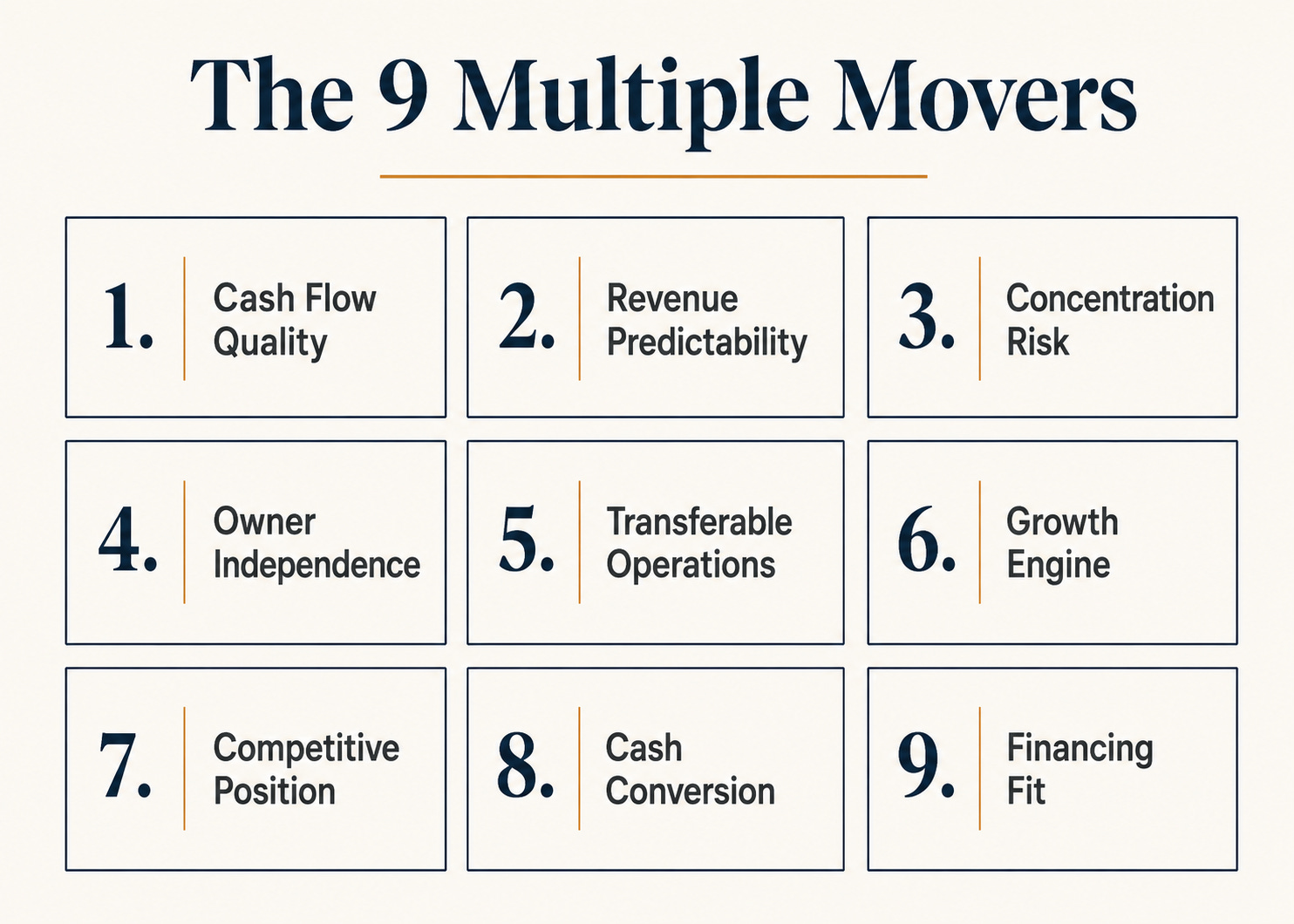

Nine company-specific factors decide where it lands. The 9 Multiple Movers.

For owners, this decides whether years of building pay off. For buyers, it decides whether the business holds up for years to come.

The janitorial company had $650,000 in seller’s discretionary earnings. The asking price was $2.8 million, right near the top of the industry range. After some back and forth, they agreed to $2.6 million all cash on close.

We spent two weeks in due diligence before flagging a few things.

Three customers made up 39% of the company’s revenue. That’s a bit scary.

Roughly 40% of monthly revenue was out of contract running month-to-month. Well below industry norms.

Documented processes were minimal. The owner ran daily operations from memory. Nothing critical was written down anywhere.

Those three things have names. Concentration Risk. Revenue Predictability. Transferable Operations. And there are 9 of them in total.

I call them “Multiple Movers.”

Together, they determine where a business actually lands inside its industry multiple range. And they are a proxy for the risk associated with any acquisition.

In this deal, the buyer had a choice: renegotiate the price and/or restructure the terms. They chose terms.

$700,000 moved from SBA financing to a forgivable seller note, structured around 12-month customer retention tranches. If 90% or more of the revenue stayed on the books for a year, the seller collected the full note. Below 75% retention, the note was fully forgiven. In between those thresholds, the note was partially written off.

The transition period was extended from 30 days of mostly part-time to a 90-day full-time commitment and extended availability throughout the first year. During that time, the outgoing owner needed to transition key relationships and help document key processes.

The buyer built a structure where the three things they were worried about had real financial consequences for the person best positioned to manage them through the transition: the outgoing owner.

Both sides got what they needed. The buyer felt comfortable with the risk identified during due diligence. And the seller wound up getting every dollar of the headline price.

Most owners know where the cash flow lever is. They can see it on the P&L. Grow revenue, cut costs, watch the number move. The math is straightforward.

The multiple is a different kind of lever. It sits on top of the earnings base, and it is the bigger lever on final price. On a business generating $1M in cash flow, the difference between a 3x and a 5x multiple is $2M.

That gap does not come from the industry range. It comes from 9 company-specific factors.

Here they are:

Cash Flow Quality. Owners value the business off what shows up on the P&L. Buyers value it off what survives diligence. Cash flow quality drives everything else. A weak score on this Mover discounts every other Mover with it.

Revenue Predictability. Recurring revenue and multi-year contracts reduce perceived risk of future shortfalls. Month-to-month or project-based revenue is common. Guaranteed revenue is worth more, and buyers will pay more for it.

Concentration Risk. When a significant share of revenue depends on a small number of customers, suppliers, or employees, buyers associate that with additional risk. The response shows up sometimes in the multiple, often in deal structure.

Owner Independence. Buyers can tell the difference between an operating company and an owner’s job. When the business runs on the owner’s daily presence, the buyer has to replace the owner before collecting cash flow.

Transferable Operations. Documented processes and institutional knowledge that live in the company rather than in the owner’s head reduce transition risk for the buyer.

Growth Engine. A repeatable mechanism for generating new customers is valued differently than growth that depends on the owner calling the right people, or single channel marketing.

Competitive Position. The bar is lower here than most owners expect. Most sub-$10M businesses do not have a defensible moat. Proprietary product, exclusive territory, or long-term sticky customers are legitimate positions. Generic service businesses without switching costs sit at the lower end.

Cash Conversion. High inventory requirements, long receivables cycles, or capital-intensive operations eat into reported cash flow. The question is how much of the earnings number a buyer can actually collect.

Financing Fit. Whether the deal can be funded at the seller’s price. Bank underwriting, debt cash flow coverage, seller financing capacity, and alternative funding sources all shape the universe of buyers who can actually close.

No single Mover decides where a business lands. The 9 work together, and they compound. A business with three strong Movers and six weak ones does not average out to the middle of the range. The weak ones pull harder than the strong ones push.

It works the same in every deal.

Strong Movers lower risk. Weak Movers increase it.

These impact the multiple, the deal structure, or both. Here are two deals that show this clearly from opposite directions.

Seven months of focused work

A landscaping company with $1.2M in EBITDA. The industry multiple at this cash flow level ranges from about a 3.5-5.5x. At the low end of that range, the owner walks away with $4.2M. At the high end, $6.6M. The difference between those numbers is why the Multiple Movers matter.

When the owner approached me, he had two big issues. Owner Independence was the bigger one. The owner ran day-to-day operations and personally managed the company’s most important client relationships.

This business ran on the owner’s back. He was in every client relationship and every operational decision. From a buyer’s perspective, that was a job, not a business.

Revenue Predictability was the other weak Mover. Most of the major account revenue was month-to-month. No contracts locking in the work going forward.

Seven months of focused work and we were finally ready to go to market. The owner hired a VP of Operations and stepped back from running day-to-day. A senior salesperson took over the major account relationships. The larger commercial accounts moved to multi-year contracts.

No new business lines. No huge marketing campaigns. No dramatic operational overhaul. The work was focused on fixing Owner Independence and Revenue Predictability, moving them from weak to something a buyer could look at favorably.

The outcome: he sold at 4.9x. Much more than he would have received had he not spent a relatively short amount of time fixing these issues.

Your Price, My Terms

The janitorial deal from earlier went the other direction. Due diligence flagged three weak Movers: Concentration Risk, Revenue Predictability, and Transferable Operations.

The buyer didn’t try and re-negotiate the price. That’s always a delicate subject. Instead, he proposed terms that would mitigate the risks while offering the seller an opportunity to prove the business was worth what he thought it was.

The Myth of the Multiple

People often get a specific multiple number stuck in their head. And that often comes from an industry average they’ve read about or stories about other deals that closed.

But that’s not the best way of thinking about it.

Instead, think of it as a range that a business will likely sell for. Where a business lands inside that range is decided by the nine Multiple Movers.

Strong Movers push toward the top. Weak Movers pull toward the bottom, or move the risk into the deal structure when buyers decide the price isn’t worth fighting.

For the owner, weak Movers are a direct cost. For the buyer, weak Movers are a red flag. The same diagnostic reads differently from each side of the table, but the underlying mechanism doesn’t change.

The question, for both sides, is which Movers are actually weak and what it would take to move them.

For the owner, the starting question is which Movers are actually weak and which ones can be moved in the time available. Four of the nine come up most often in that conversation. The other five still matter, but they don’t usually move much within a planning horizon.

Cash Flow Quality sits at the foundation. When it’s weak, the doubt it creates tends to follow every other Mover. Strong Revenue Predictability matters less if the buyer isn’t sure what earnings base to apply it to. Transferable Operations look better on paper than they perform in diligence. The buyer prices the uncertainty, not the stated upside. Fix Cash Flow Quality first, or work on the others with that ceiling already in mind.

Transferable Operations is usually the most fixable on a reasonable timeline. Documented processes, defined roles, systems that don’t live in someone’s head: this is work that can actually be done in a few months. It doesn’t require landing new customers or restructuring the org chart. It requires execution.

Concentration Risk takes longer. Diversifying a customer base, building redundancy in key supplier relationships, reducing the dependence on any single employee. That’s going to take some time. An owner who wants to go to market within the next six to twelve months can make some improvements but they need to be realistic about the potential impact.

Owner Independence tends to be the highest-leverage work when there’s real runway before the sale. Hiring into the business, transitioning relationships, proving the team can run things. Buyers test this against observed behavior, not stated intent. That takes time. An owner who starts early on this can make a significant impact on the multiple and the amount of cash they put in their pocket.

For the buyer, the diagnostic flips. The question isn’t which Movers are fixable. It’s whether the price on the table reflects the Movers that are actually weak, and whether they can accept the risk that comes with them.

When a deal is priced at the top of the multiple range and comes with a host of weak Movers, it’s overpriced. But when a buyer finds a strong business with strong Movers, even a mid-range price might be an amazing deal.

Four of the nine Multiple Movers tend to come up most often in due diligence. The other five aren’t ignored, they just show up less often.

Cash Flow Quality is where every buyer’s diligence starts. If add-backs don’t hold up, if margins are unstable, or if revenue recognition is messy, the buyer has to make a choice. Apply a lower multiple to a lower cash flow number, offer risk mitigating terms, or walk away. Cash Flow Quality is what decides whether the rest of the due diligence is even worth doing.

Concentration Risk is the Mover most likely to hide in a strong recent year. A business with 35% of revenue from one customer can post twelve good months and still carry serious risk into the next year. The buyer’s job is to look forward and ask what happens if that customer leaves. The answer ends up in the price or the structure.

Financing Fit is mostly buyer-side execution. The seller knows the price they want; the buyer has to figure out how to get there with bank underwriting, seller financing, and the equity infusion available. Weak Financing Fit forces creative structure to bridge the gap when the lender’s number and the seller’s number don’t agree.

Cash Conversion is where reported earnings stop being theoretical. Working capital, receivables cycles, and capital expenditures all consume cash before it shows up in the bank account. A business that shows strong EBITDA but burns cash to grow is a different deal than one that converts earnings cleanly. Debt service has to come from somewhere.

The harder case is when the discount isn’t in the price at all. A deal can be priced at a reasonable multiple and still carry significant risk if the Movers aren’t examined.

That risk doesn’t disappear because the price looked fair. It comes with the deal. The Movers are what separate a fair price on a strong business from a fair price on a fragile one, and a sharp buyer treats that distinction as the whole point.

Buying a business is one of the biggest moves a person makes with their capital. Done well, it can change a life. The Multiple Movers are how a sharp buyer separates the deals worth that move from the ones that aren’t.

When both sides are working from the same framework, the surprises mostly go away. The owner knows what the buyer is looking for. The buyer knows what the owner has strengthened.

The owner gets paid for the work they did. The buyer acquires a business they can build on. Both sides win when both sides see the same picture.

Two levers move the price on an acquisition.

The first is cash flow. Grow the earnings base and the price goes up. It shows up on the P&L every month. Visible, trackable, and something most owners work on for their entire careers.

The second lever is the multiple that sits on top of that earnings base and how the business measures up against its peers in terms of risk. In an industry priced between 3.5x and 6x, the gap between those two endpoints is massive. On a $1.2M EBITDA business, it is more than $3 million.

Both levers are real. The cash flow lever is the one most owners ponder day and night. The multiple lever is the one most owners don’t even think about.

The 9 Multiple Movers are the key.

Cash Flow Quality, Revenue Predictability, Concentration Risk, Owner Independence, Transferable Operations, Growth Engine, Competitive Position, Cash Conversion, Financing Fit.

Each one either lowers perceived risk or raises it. Strong Movers push a business toward higher multiples, higher offers, and seller-favorable terms. Weak ones push it to lower multiples, lower offers, and buyer-favorable terms.

If you’re an owner, this is what decides whether the next chapter of your life looks like the one you spent years imagining.

If you’re a buyer, this is how you commit to your next chapter knowing the business will actually hold up for years to come.

If this landed, share it with someone facing a decision like this on either side of the table.

If you’re working through it yourself, I read every reply.